Most contractors I talk to fall into one of two groups. Either they don’t know what to provide their bookkeeper at month end, or worse, their bookkeeper produces a Work in Progress report (WIP), and they don’t know what it means. In both cases, the problem isn’t accounting. The problem is ownership of information.

If production doesn’t own cost to complete, accounting can’t produce a meaningful WIP. And if the WIP isn’t meaningful, your month-end close— the process of finalizing the books so the financial statements reflect what actually happened that month—is little more than a guess.

Over the past few years, as I’ve stepped into what I think of as the CFO of Production role at our company, I’ve come to see month-end close and the WIP very differently. They are not simply bookkeeping artifacts. Viewed correctly, they can be management tools. And like all good tools, their usefulness depends entirely on the quality of the inputs, especially cost to complete.

Month-End Close

Before talking about the WIP or cost to complete, it’s worth clarifying why we close the month at all. The purpose of month-end close is not compliance and it’s not to satisfy your CPA. It’s to answer three questions with confidence:

- How much revenue did we earn this month?

- How much gross profit did that revenue generate?

- What decisions can we safely make next month?

If you don’t trust the answers, you’re running the business on last month’s weather report. That’s how companies drift into cash flow surprises, over-hire labor, or green-light projects they can’t support.

For companies with long-duration projects, the accuracy of month-end accounting lives and dies by the WIP. And the accuracy of the WIP lives and dies by cost to complete.

WIP: Fundamentally an Accounting Tool

A WIP is a monthly financial snapshot that shows how much revenue and profit a contractor has truly earned on each active job, based on actual costs and progress. For instance, it might show that the contractor has incurred and billed for $60,000 in costs on a kitchen remodel with an estimated job cost of $80,000. Assuming the job is performing to its estimate, the cost to complete is $20,000.

There’s a tendency among production leaders to want the WIP to provide forecasting, schedule validation, and labor analysis. In my experience, that insight already exists upstream in accurate job costing and cost to complete tracking.

The WIP’s job is narrower and that’s a good thing. Its primary purpose is to present an accurate picture of earned revenue and over- or under-billings at a point in time. In the above example, if the contractor has billed the client $70,000 the project is $10,000 overbilled while $50,000 in billings would result in a $10,000 underbilling. When cost to complete is solid, the WIP does that job extremely well. When it isn’t, producing the WIP becomes accounting gymnastics. (For more on generating accurate WIP reports, see Melanie Hodgdon’s “Recognizing Earned Income,” 5/23, and “Process vs. Purpose: The Key to Accurate WIP Adjustments,” 7/25.)

Cost to Complete: Where Reality Enters Accounting

Cost to complete, or CTC, is the single most important input to an accurate WIP. Again, in my view, WIP is fundamentally an accounting tool designed to reconcile earned revenue and identify over- or under-billings. But the quality of that reconciliation depends entirely on whether CTC reflects reality in the field.

At our company, CTC is owned by the Project Manager. When a PM marks a line item “complete” in our job costing system, they are making a very specific judgment: no additional meaningful costs—only those less than $1000—remain on that scope. That judgment isn’t based on a formula. It’s based on the PM using their knowledge of scope, labor performance, and trade partner invoicing to record costs against an estimate set up with job costing in mind.

Some job costing programs or spreadsheets allow you to give a line item a specific completion percentage, but JobTread, the program we use at TDS, only allows a done/not done input. At first this limited our CTC effectiveness until we devised a system of using internal change orders to add cost to the project estimate. CTC is not about being right at bid time; it’s about being honest as reality unfolds.

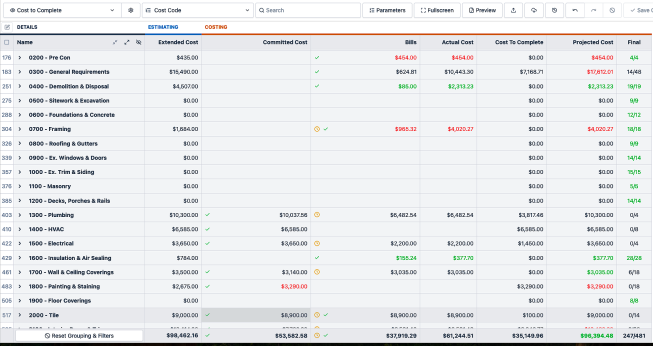

Click to enlarge image below.

The JobTread cost to complete budget view provides the cost to complete adjustment for the WIP by subtracting the bills in real time from the estimated project cost. All change orders, including internal ones, are accounted for in the extended cost.

Effect of Change Orders

When we become aware of additional costs we add them to the job immediately. Sometimes there’s margin attached. Sometimes there isn’t. Either way, the job’s cost structure reflects what we now know to be true today, not on the day the project was sold.

I believe that this is where many companies go wrong. They delay acknowledging cost changes in the hope that labor will make it up later. All that does is distort CTC, which then distorts the WIP, which then distorts revenue recognition on the P&L. By the time the job finishes, the financials tell a story no one recognizes.

That’s why internal change orders are important. They keep CTC honest, which keeps the WIP accurate.

Early Warning System

One advantage of accurate cost to complete is that it acts as an early warning system. In our work, when both demolition and framing start trending over cost, often by the one-third mark of the job, it’s a signal that something deeper is off.

Sometimes it’s an estimating error. Sometimes it’s poor scope definition. Occasionally it’s a macro trend, such as an unexpected increase in material costs, that needs to feed back into future estimates.

Production leadership cannot rely on accounting to discover these trends. Accounting’s role is to use the data provided by production to report on the consequences of company performance.

Before Closing Out the Month

At our company, we won’t close the month until three things happen:

- All bills and invoices have been processed through job costing.

- Cost to complete has been updated.

- Production leadership agrees that the numbers reflect reality.

Without this discipline the damage shows up immediately: incorrect over- or under-billings, revenue pulled forward or delayed, and a P&L that doesn’t match what’s happening in the field.

GP/Day and VPW Live Inside WIP

Although WIP doesn’t explicitly reference metrics like Gross Profit per Day (GP/Day) or Volume per Week (VPW), they’re embedded in it. Each month’s WIP shows total earned gross profit and revenue.

Using the spreadsheet to calculate the monthly differences allows you to track other performance metrics. Divide earned gross profit by the days in the month and you have GP/Day. Earned revenue divided by the number of weeks gives you VPW.

In that sense, WIP doesn’t replace operational metrics; it validates them. It proves whether your assumptions about duration, throughput, and labor efficiency were right.

A Production Leader’s Read

When I review the WIP, I’m not hunting for accounting errors. I’m asking production questions. If we’re over-billed, did we receive a large deposit this month? If we’re under-billed, who owes us money and why? Every answer ties back to billing timing, production progress, and cost to complete confidence.

WIP doesn’t fix problems. It reflects how well production and leadership are aligned. If your WIP is confusing, the problem isn’t accounting. It’s that production hasn’t finished telling the story yet or doesn’t know how to tell it. CTC is where reality enters the financial system. When production and accounting own their inputs then month-end close becomes a management exercise instead of a mystery.